Seller Credits & Closing Costs on the Westside

Seller Credits & Closing Costs on the Westside

by Les Goss

If you’re close to buying or selling in Colorado Springs—especially the Westside—this is the moment where deals are won or lost on the details. Not the “headline market.”

The two biggest decision-stage stressors I’m hearing right now are: (1) cash-to-close clarity and (2) negotiation leverage—especially whether a seller can help cover closing costs or a rate buydown.

Below is the practical, Westside-specific guide: what’s negotiable, what’s capped by loan rules, and how to use ZIP-level signals to know when to push.

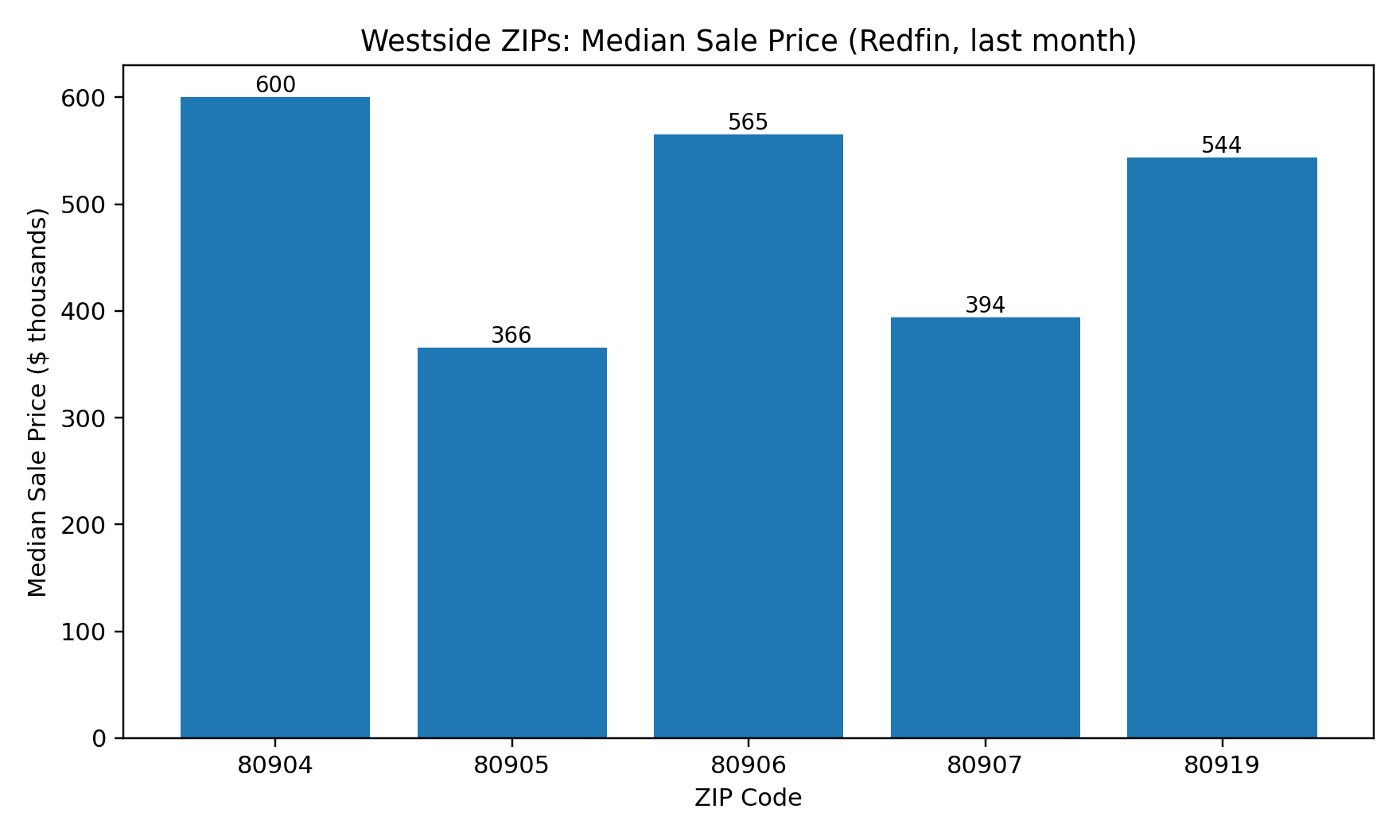

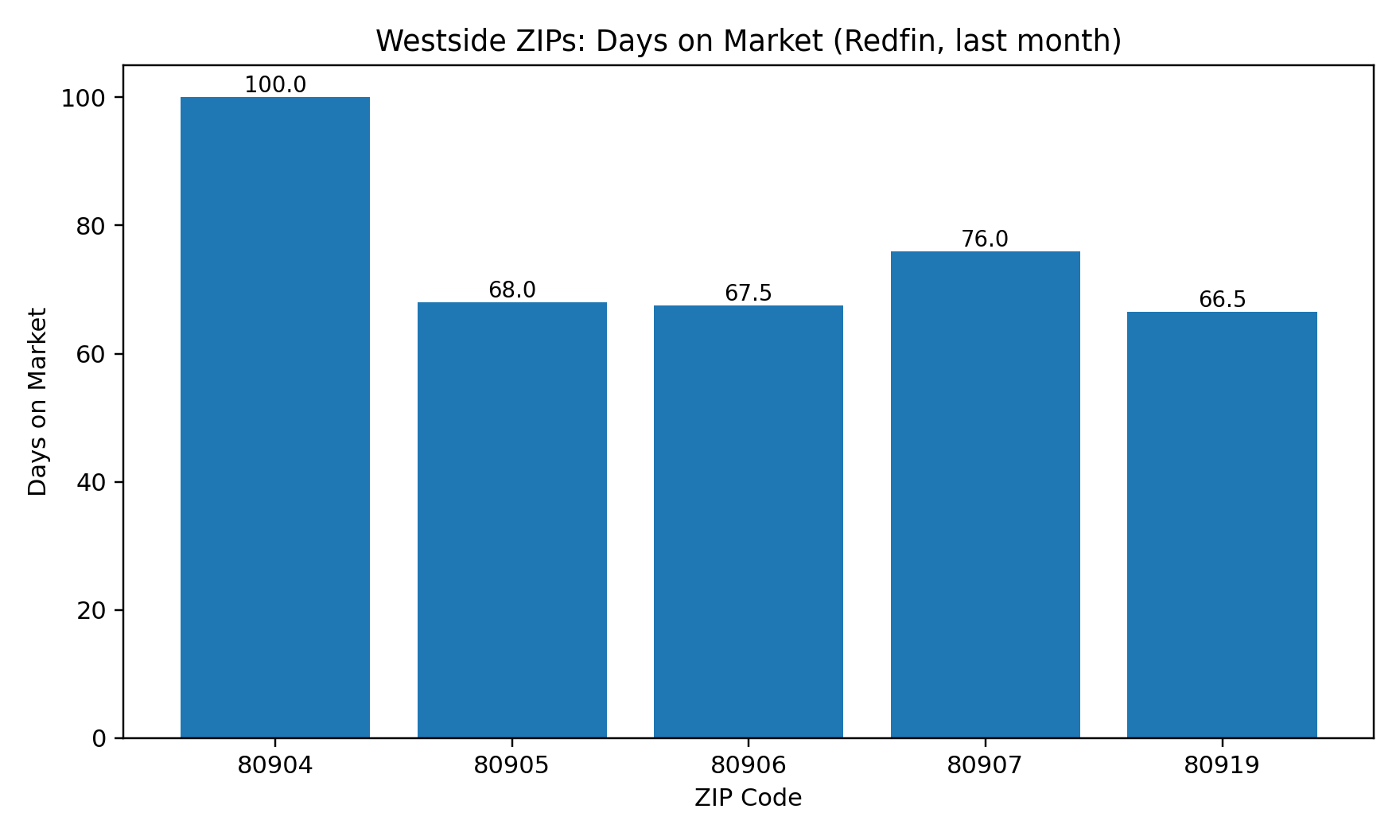

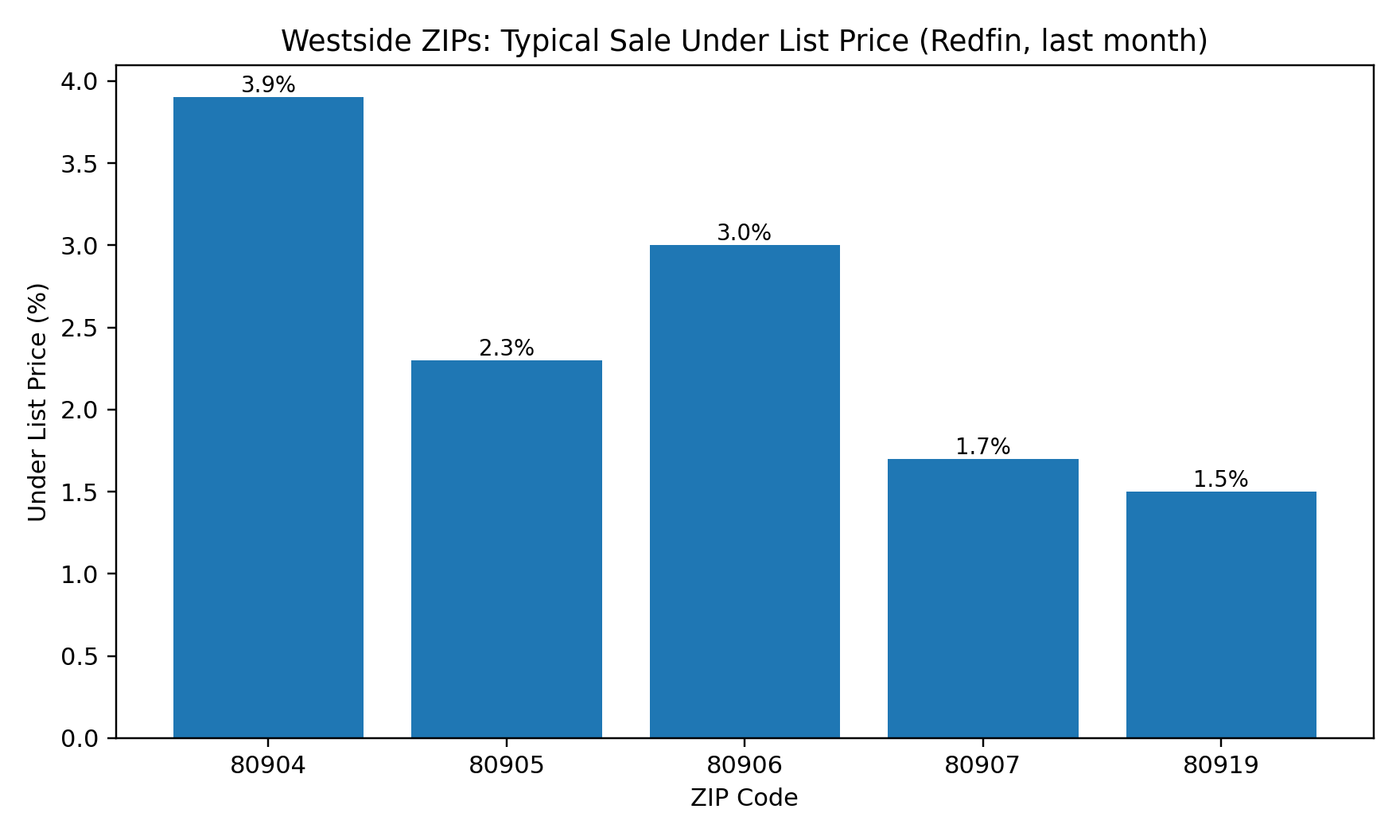

Quick Westside reality check: leverage is ZIP-specific

Colorado Springs overall is moving at a measured pace (about 72 days on market in a recent snapshot). PPAR’s most recent market snapshot also shows 71 average days on market with a $449K median in the latest posted snapshot period.

- 80904: ~100 DOM; ~3.9% under list price

- 80905: ~68 DOM; ~2.3% under list price

- 80906: ~67.5 DOM; ~3.0% under list price

- 80907: ~76 DOM; ~1.7% under list price

- 80919: ~66.5 DOM; ~1.5% under list price

Translation: some Westside pockets are giving buyers more room to negotiate credits or repairs, while others are closer to “pay attention—this one can still move.”

Question #1: Can a seller cover my closing costs?

Yes—often through a seller credit—but there are two filters that matter:

- Market leverage: Do the ZIP-level signals support concessions (DOM, under-list trends, competition)?

- Loan rules: Conventional loans have limits on “interested party contributions.”

For many conventional loans (Fannie Mae guidance), maximum concessions can be:

- 3% when LTV > 90% (low down payment)

- 6% when LTV is 75.01%–90%

- 9% when LTV ≤ 75%

- 2% for investment properties

This is why a good buyer strategy isn’t just “ask for $10K.” It’s: structure the offer so the credit is allowable, appraisable, and actually helps the payment or cash-to-close.

Question #2: What exactly is included in “cash to close”?

“Closing costs” are not one line item. The cleanest way to stay in control is to use two standardized documents:

- Loan Estimate: early breakdown of loan terms, closing costs, and estimated cash to close.

- Closing Disclosure: final five-page breakdown of the exact costs and terms you’ll sign.

The CFPB’s guidance is simple and powerful: compare the Cash to Close number on your Closing Disclosure to your most recent Loan Estimate, and ask your lender about any significant changes.

If you’re relocating (or moving up and juggling timing), this is the moment to tighten the plan: lender, agent, and title all aligned so the numbers don’t surprise you in the final week.

Question #3: Should I negotiate price or negotiate credits?

Here’s the practical answer: it depends on what your bottleneck is.

- If your bottleneck is monthly payment: a credit that supports a rate buydown (if lender allows) can sometimes be more valuable than a small price cut.

- If your bottleneck is appraisal risk: credits can be safer than aggressive pricing (especially if the home is unique).

- If your bottleneck is “net proceeds” as a seller: credits may feel easier than a price reduction—but only if they still close cleanly.

ZIP-level signals help you decide how hard to push. For example, areas showing deeper “under list” behavior tend to support stronger credit negotiations—while tighter pockets may require cleaner offers.

Question #4: How do I win on the Westside without overpaying?

Two ways:

- Be the easiest buyer to say “yes” to: strong pre-approval, clear timeline, thoughtful concessions request that fits loan rules.

- Stop only shopping what everyone else can see: build a Westside target list and create off-market conversations.

That’s where my target marketing approach comes in. Instead of waiting for the perfect home to hit the MLS, we define the micro-area (streets and pockets that match your lifestyle), then use strategic outreach to connect with owners who would consider a move for the right buyer.

Boomers downsizing: protect net proceeds and avoid surprises

If you’re 60+ and thinking about a downsizing move, your biggest win is usually a calm, coordinated plan: pricing strategy, timing, and a clear picture of net proceeds.

Tax rules vary by situation, but many homeowners may qualify to exclude up to $250,000 of gain (single) or $500,000 (married filing jointly) on the sale of a primary residence if requirements are met. Always confirm with a tax professional.

Call to Action: want a Westside “offer + cash-to-close” plan?

If you’re within 90 days of buying or selling on the Westside, send me your ZIP + price range + timing.

- Buyers: I’ll map a negotiation plan (price vs credit) that fits your loan rules and your cash-to-close target—plus an off-market target list if you want to widen inventory.

- Sellers: I’ll build a net sheet + timing plan and show you what concessions (if any) actually help you sell faster without giving away the farm.

Categories

Recent Posts

REVIEWS

Dave Brackett

GET MORE INFORMATION